A List Of Ten Common Accounting Terms Explained

If we talk about accounting then the first thing that comes to our mind is “Debit what comes in and credit what goes out” Accounting is more than that, it is the most important study to find out the profit or the loss in the business, earning and expenditure in a company, debit, and credit of the money. Here are some of the basic terms used in accounting:

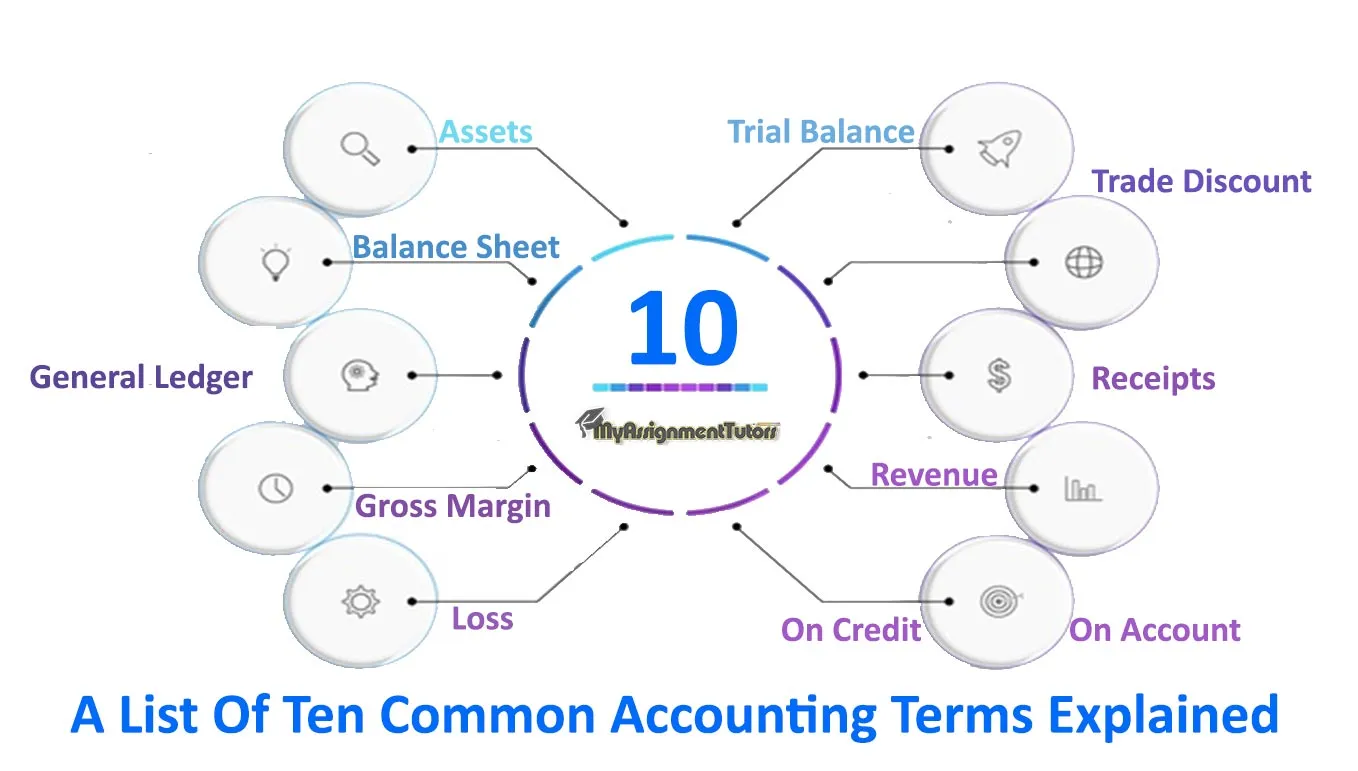

Common Accounting Terms

- Assets: Assets area unit the wealth that has been accumulated by the business and is owned outright while not lien or loan. It’s going to be things that depreciate over time or products that area unit oversubscribed to customers. This could embrace money and investments, buildings and property, assets, warehouse inventory, instrumentation, and provides.

- Balance Sheet: The record is a very important side of the business. It records the fundamental accounting formula of assets = liabilities + shareholder equity/capital at an exact purpose in time, either monthly, quarterly, or yearly. From the record, the monetary health of the business will be observed.

- General Ledger: The general ledger is that the facet of the accounting ledger that contains the record and also the statement accounts. Here all business transactions area unit recorded, as well as sales, credit purchases, workplace expenses, and financial gain losses.

- Gross Margin: Gross margin or profit is that the total range of sales that are created, deducted by the associated prices, like producing prices, wholesale prices, material, and provides.

- Loss: When a service or product sells for less than what it value to produce or manufacture it, or once expenses have exceeded revenues of selected quality, it's referred to as a loss.

- On credit/on account: On credit or account implies that merchandise or services are oversubscribed with the utilization of credit. Payment has not in real-time been provided for these things, and there could also be terms on account that will lead to interest charges.

- Receipts: Receipts are that the total quantity of money collected in business transactions over 1 day. It doesn't embrace alternative revenue collected.

- Revenue: Income and revenue area unit interchangeable, compromising the entire quantity of all financial gain collected at one purpose in time. It’s going to embrace money sales, credit purchases, and subscription fees, and interest financial gain. It differs from receipts because it will embrace monies that don't seem to be collected at the delivery time.

- Trade Discount: A deduction may be a share discounted from the acquisition value and is predicated on the number of products ordered at one purpose in time. Higher discounts could also apply to larger orders, with smaller discounts for lesser orders.

- Trial Balance: The balance is recorded within the account book and includes each debit and credit for one explicit account. The sheet should balance, with debits equaling credits.

Conclusion

In the above article, the readers will learn about the basic accounting term which should be known to all the citizens who maintain the record of earning as well as expenditure. If you need help in accounting assignments then contact Myassignmenttutors.com.